Tokenized real-world assets (RWAs) have surpassed $35 billion in total value as of November 2025, according to data from rwa.xyz. This represents a notable inflection point in the development of tokenized markets, underscoring the increased involvement of institutional players, expanded use cases, and regulatory engagement across major jurisdictions.

In this article, we explore what’s driving the growth of tokenized real-world assets past the $35 billion mark and what challenges remain.

Key Takeaways

- Tokenized RWAs have reached $35.9B in value, growing ~131% year-to-date, with private credit and Treasuries leading adoption.

- Private credit comprises over $18.91B in active value, reflecting demand for on-chain yield instruments with defined terms and structures.

- Tokenized U.S. Treasuries have surpassed $9B, serving as blockchain-native alternatives to traditional money market products.

- New use cases, including tokenized equities, R&D assets, and IP rights, are gaining traction across multiple jurisdictions.

- Challenges persist in standardization, legal clarity, and global regulatory alignment, with global entities like MAS and OECD highlighting the need for interoperable networks and safe settlement assets.

Tokenized Market Size: Where We Are Now

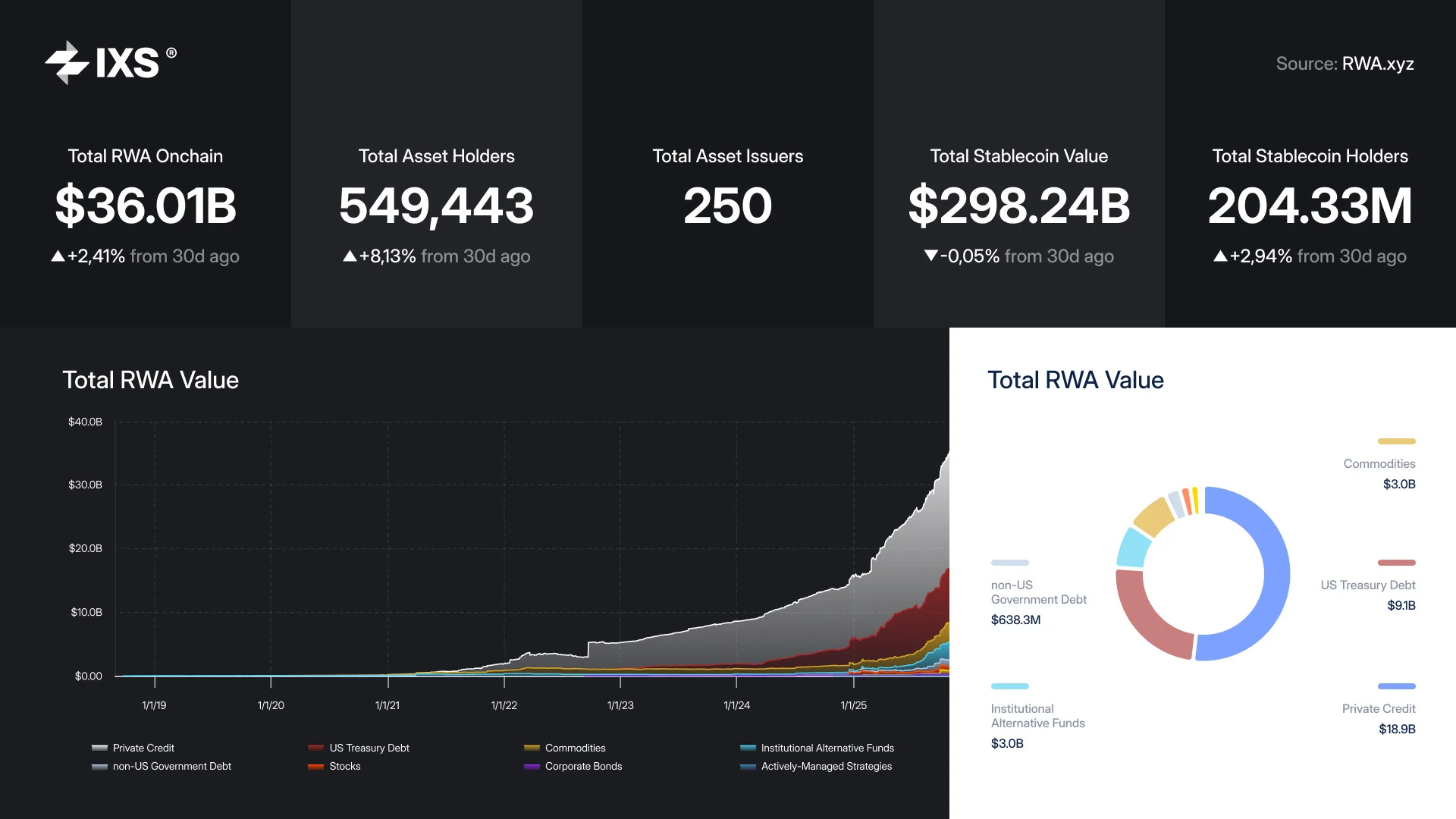

As of November 2025, the tokenized RWA market reached $36 billion, representing an increase of approximately 131% year-to-date, according to rwa.xyz. This figure reflects real-time on-chain data across permissioned and public networks, covering assets from Treasuries and private credit to tokenized gold and real estate.

Top Tokenized Asset Categories as of November 2025:

- Private Credit: With over $18.91 billion in active value and $33.66 billion in cumulative originations, private credit remains the largest category in tokenized RWAs. Platforms such as Maple, Centrifuge, and Goldfinch are key issuers, with structures ranging from senior secured loans to SME credit pools. Borrower-side yields typically range between 8-12%. Source

- U.S. Treasuries: Tokenized Treasury bills have gained strong traction, particularly as blockchain-native alternatives to traditional money market products. As of November 2025, the tokenized U.S. Treasuries category exceeds $9 billion in tokenized value. Protocols like Securitize, Ondo Finance, and Circle dominate issuance, primarily offering short-dated U.S. Treasury exposure as on-chain yield instruments. Source

- Commodities: Tokenized commodities exceeded $3.5 billion in total value as of November 2025. Gold remains the dominant underlying in this segment, with PAXG and XAUT together representing more than $2.9 billion in tokenized gold in circulation, accounting for over 80% of the total tokenized commodity market. Source.

- Institutional Alternative Funds: Institutional alternative investment vehicles are now represented on-chain through tokenized feeder structures and fund units. As of November 2025, the category has reached $2.95B in total value. Notable examples include JAAA - a tokenized representation of the Janus Henderson AAA CLO ETF, offering exposure to investment-grade CLO tranches and USCC - issued by Superstate, providing tokenized access to a short-duration U.S. government securities fund.

Key Trends Behind the $35 B+ Milestone

The acceleration of tokenized RWA adoption in 2025 appears to be shaped by several reinforcing market and infrastructure trends. Below are some of the most observable contributors based on available data and active platforms:

1. Flight to quality amid macro uncertainty

Tokenized U.S. Treasuries have grown to over $9 billion in value as of November 2025. Their availability on-chain, alongside existing custody and compliance mechanisms has made them accessible to investors already familiar with these instruments. This has supported adoption, particularly among those seeking predictable yield within programmable digital formats.

2. Institutional entry via compliant issuance

Veteran financial firms such as Franklin Templeton, OCBC, and GuoFu Quantum are issuing tokenized assets under licensed frameworks, improving institutional comfort and expanding compliant distribution.

3. Regulated DeFi integrations and real-yield architectures

Some tokenized RWAs are now linked to yield strategies structured within regulated environments. For example, the IXS BTC Real Yield product enables institutional BTC holders to earn stablecoin-denominated returns by pledging BTC into non-recourse loan structures. These stablecoins are then deployed into short-term, regulated fixed income instruments, such as Treasuries or corporate credit, delivering 4-10% APY annually without liquidating the original BTC position.

4. Infrastructure maturity: custody, issuance, and transfer

Growth has also been supported by improvements in custody, compliance, and lifecycle management tools. Institutional-grade custodians (e.g., Anchorage, BitGo, Fireblocks) now offer segregated RWA custody services, while end to end RWA issuance platforms like IXS, InvestaX, and Securitize provide issuance, distribution and secondary trading of tokenized assets.

New Use Cases Gaining Traction

Beyond the major categories such as Treasuries and private credit, tokenization has been extending into sectors like stocks, R&D assets and IP assets. Adoption varies by jurisdiction and regulatory maturity, but several segments show measurable activity and institutional interest.

1. Tokenized U.S. equities

The concept of digital tokens representing shares of publicly listed companies is an emerging trend in asset tokenization. In 2025, major platforms announced or expanded tokenized equity initiatives:

- Robinhood + Bitpanda: Developing tokenized stock offerings for 24/7 trading with compliant transfer restrictions.

- Coinbase: Reportedly piloting tokenized equity infrastructure as part of its institutional asset tokenization strategy.

- Kraken and Gemini: Exploring tokenized securities through regulated subsidiaries.

Bybit: Supporting synthetic tokenized stock products in parallel to regulated markets. - Nasdaq: Filed to enable blockchain-based tokenized securities trading on its primary markets - the strongest signal yet that tokenized equities may become part of mainstream market infrastructure.

2. Energy infrastructure in China

Ant Digital Technologies (part of Ant Group) has initiated tokenisation of approximately US$8.4 billion of renewable energy assets on its proprietary blockchain network. The project tracks over 15 million devices and is building a foundation for digital claims on infrastructure cash flows. Cointelegraph

3. Tokenized Real Estate

Real estate tokenization continues to accelerate with major developments observed in the UAE, Japan and other countries.

- In Japan, Mitsubishi UFJ Trust & Banking Corporation is planning to tokenize real estate assets and make them available to both retail and institutional segments. This illustrates how markets that have traditionally excluded non‑institutions are experimenting with new models to expand access.

- In the UAE, MultiBank Group, MAG, and Mavryk have signed an agreement to tokenize $3 billion worth of UAE-based luxury real estate. Cointelegraph.

- Trump Organization announced its plan to tokenize new Maldives luxury resort, in collaboration with Dar Global (LSE: DAR).

4. Pharma and R&D financing

Tokenization is being explored in biotech and R&D, particularly for long-cycle development assets.

Example: IVD Medical Holding partnered with Transcenta to tokenize revenue-linked claims tied to drug development milestones.

These structures create programmable distributions and transparent tracking of development progress, expanding tokenization beyond conventional financial assets.

5. Intellectual property (IP) and media rights

Tokenization is increasingly used for rights management, transparent revenue participation, and fractional media financing.

A practical example is the feature film “Demon Hunters: Confession”, structured on IXS as a tokenized media property:

- Ownership rights and revenue-share claims are formalized via digital security tokens.

- Governance, compliance, and reporting processes are embedded at the token level.

- Investors gain access to previously opaque IP-backed revenue streams.

These examples indicate that tokenisation is expanding beyond incremental asset classes into novel sectors. While many of these models remain nascent, their registration and pilot status signal increasing institutional appetite, infrastructure readiness and regulatory engagement.

Remaining Challenges to Watch

While tokenization continues to gain traction, several areas still require further development before tokenization can scale sustainably. These considerations have been raised consistently by both regulators and industry participants in 2025, including the Monetary Authority of Singapore (MAS) and the OECD.

At the Singapore FinTech Festival 2025, MAS Managing Director Mr. Chia Der Jiun highlighted three areas where further development is needed: greater standardization of asset-backed tokens, interoperable infrastructure, and access to deep, reliable settlement assets (MAS, 2025). Meanwhile, the OECD’s report “Tokenisation of assets and distributed ledger technologies in financial markets: Potential impediments to market development and policy implications” pointed to legal, operational, limited secondary market activity and jurisdictional challenges as key factors influencing the pace of development (OECD, 2025).

1. Standardization and Interoperability

Tokenized assets today are issued across a diverse range of blockchain networks, including Ethereum, Polygon, Stellar, Avalanche, and permissioned ledgers such as Provenance. Each ecosystem supports different token standards, data structures, and compliance models, which can make lifecycle tracking, reporting, and transferability less seamless than conventional systems.

The OECD notes that this lack of interoperability contributes to fragmentation in tokenized markets, with limited ability to execute across platforms or enforce shared standards for asset metadata, risk, or identity. While global initiatives such as ISO’s Digital Token Identifier (DTI) and the InterWork Alliance’s token taxonomy are beginning to gain traction, their adoption remains early-stage. Cross-chain protocols such as Chainlink CCIP and pilot programs like Switzerland’s Project Helvetia offer promising direction, but broader convergence remains a work in progress.

2. Settlement Asset Depth and Reliability

Settlement remains a central concern for tokenized markets. While stablecoins are widely used within digital asset ecosystems, their structures and legal treatment vary significantly across jurisdictions. Some are regulated as e-money; others operate under less formal standards. Differences in reserve transparency, redemption terms, and on-chain liquidity have made it more difficult to rely on them as institutional-grade settlement assets.

CBDCs are often viewed as a long-term solution, but adoption is still limited. According to the OECD, more than 60% of central banks surveyed are not currently authorized to issue token-based CBDCs, and most programs remain at the pilot or consultation stage. In the meantime, workarounds - such as tokenized Treasury products or regulated fiat-backed stablecoins - provide partial solutions, though legal enforceability and systemic scalability vary by product.

3. Institutional-Grade Networks and Market Design

The platforms supporting tokenized assets have evolved significantly in recent years, yet challenges persist around infrastructure maturity and design choices. Many tokenized products are issued on public blockchains with smart contract-based compliance layers, or within permissioned environments with limited composability. Both models carry tradeoffs. The OECD notes that some permissioned systems risk reproducing traditional financial silos, potentially diminishing the net efficiency gains of tokenization.

Institutional participants have also highlighted concerns around fragmented liquidity, onboarding complexity for custodians, and ambiguity around token-holder rights in situations such as insolvency or cross-border disputes. Several jurisdictions are responding with regulatory sandboxes, such as the UK’s Digital Securities Sandbox, to enable controlled experimentation with settlement and asset servicing. Meanwhile, platforms are increasingly embedding compliance features such as dual-signatory custody, automated audit trails, and legal wrappers to address investor protection requirements.

4. Demonstrated Operational Efficiency at Scale

One of the core promises of tokenization is the potential for operational efficiency: faster settlement, reduced counterparty risk, and more transparent record-keeping. However, according to the OECD, many of these benefits remain theoretical at scale. Most projects today are in limited production or proof-of-concept phases, and real-world comparisons with traditional systems are still emerging.

That said, several early examples suggest practical value. Tokenized private credit transactions have demonstrated faster settlement cycles and improved transparency for investors. Tokenized Treasury structures now allow DAOs and fintechs to manage liquidity with programmable controls. Yet, without robust evidence of cost reductions or improved speed across broader asset classes, some institutions remain cautious in allocating further capital or infrastructure resources. The OECD underscores that demonstrable, repeatable outcomes will be important for shifting adoption from pilot to production.

5. Regulatory Fragmentation and Jurisdictional Divergence

The regulatory landscape for tokenized assets is advancing, but inconsistencies across jurisdictions continue to influence market development. As of 2025, countries vary in how they classify tokenized instruments, as securities, digital representations, or hybrid structures, leading to differences in disclosure requirements, tax treatment, and secondary trading permissions.

The OECD notes that legal frameworks remain fragmented around questions of ownership, enforceability, and investor protection. For example, how a tokenized claim is treated in bankruptcy or how rights are enforced cross-border can differ significantly between jurisdictions. Nevertheless, progress is being made. The BIS Innovation Hub continues to coordinate cross-jurisdiction CBDC pilots. IOSCO has issued principles for the oversight of crypto-asset markets and stablecoin governance. And national regulators including MAS, the SEC, BaFin, and the FCA are each working to clarify the treatment of tokenized securities and market operators.

Further convergence on legal definitions, disclosures, and enforcement mechanisms will likely support institutional confidence in cross-border participation.

6. Custodian Infrastructure and Asset Onboarding

Custody remains a fundamental layer in the tokenized asset stack - one that is still developing in sophistication and accessibility. Institutions rely on custodians not only for safekeeping, but also for asset onboarding, compliance monitoring, and corporate action execution. According to the OECD, many digital custodians focus primarily on cryptocurrency, with limited support for regulated security tokens or complex RWA instruments.

As tokenization evolves, custodians will play a more active role in bridging off-chain assets into compliant on-chain structures. This includes the ability to support dual-control wallets, validate asset provenance, integrate with regulated marketplaces, and facilitate reporting in line with institutional mandates. Several firms, including Anchorage Digital, Zodia Custody, and BitGo, have expanded their offerings, but broader standardization in roles and responsibilities may be needed to support scalable deployment.

Conclusion

The $35 billion milestone marks tangible progress in the evolution of tokenized markets, driven by institutional engagement, regulatory traction, and early signs of product-market fit. Yet meaningful scale will depend on continued development in infrastructure, interoperability, and legal alignment across jurisdictions. As frameworks mature and more operational data becomes available, tokenization is likely to shift from isolated pilots to integrated financial infrastructure, offering new pathways for capital formation, distribution, and settlement.